Product Teardown: CRED

This blog contains the major product lessons from CRED, an online credit card bill payment platform that rewards the customers for paying credit card bills.

OVERVIEW

CRED is a groundbreaking digital platform that revolutionizes credit card management. It is an exclusive members-only club designed to reward individuals for their responsible credit card bill payments while offering them a world of exclusive benefits and premium experiences.

In today's fast-paced world, managing multiple credit cards can be a daunting task. CRED steps in to simplify this process. With Cred, users gain access to a powerful platform that not only tracks their credit card spending but also provides valuable insights into their credit score.

One of the standout features of CRED is its focus on rewarding members with high CRIF scores. By making timely credit card bill payments through the app, users with excellent creditworthiness unlock exclusive rewards and privileges, enhancing their financial journey.

But CRED goes beyond just bill payments and rewards. It empowers users with tools like credit card spend tracking and management, offering a detailed analysis of their spending habits and card usage efficiency. This level of transparency and control over one's finances sets CRED apart in the digital finance landscape.

PURPOSE/ GOAL OF THE TEARDOWN

The primary goal of this product teardown is to conduct an in-depth analysis of CRED, a digital app designed for credit card management and rewards. Our focus will be on several key aspects, including User Interface/User Experience (UI/UX) design, the customer journey, user demographics, and financial performance.

ASPECTS OF THE PRODUCT TEARDOWN

UI/UX Evaluation: We aim to assess the app's user interface and user experience to understand how CRED ensures a seamless and intuitive interaction for its members. We will analyze the design, navigation, and overall usability of the app.

Customer Journey Mapping: We will map the customer journey within the app, from onboarding to daily usage and reward redemption. Understanding the flow and touchpoints will provide insights into user engagement and satisfaction.

User Base Analysis: Examining user demographics and behaviours will help us gain a clear picture of CRED’s target audience. We aim to identify who benefits most from the app and how CRED tailors its services to their needs.

Financial Performance Assessment: While limited financial data may be available, we will aim to uncover insights into CRED’s revenue models, growth strategies, and any available financial metrics that shed light on its overall success in the digital finance industry.

By achieving these objectives, we aim to provide a comprehensive teardown of CRED as a product and share valuable insights into its user-centric approach, and financial sustainability. This teardown will help us understand how CRED has positioned itself in the competitive digital finance landscape and how it continues to innovate for the benefit of its users.

INITIAL ASSESSMENT

TARGET CUSTOMERS:

CRED's target audience is a specific niche within the credit card user base. The company aims to attract individuals falling within the NCCS (New Consumer Classification System) A and NCCS B categories, which typically represent the financially well-off segment of the population. These users are expected to have access to one or more credit cards, making them potential candidates for CRED's services.

However, CRED doesn't stop at financial segmentation alone. To further refine its target customer base, the app sets a strict eligibility criterion, allowing only individuals with a CIBIL score of at least 750 to become members. This indicates a focus on customers with a strong credit history and higher creditworthiness.

KEY DEMOGRAPHICS:

Age: CRED primarily caters to individuals in the age group of 25-40. This age bracket typically represents young professionals and working-age adults who are more likely to own credit cards and engage with financial services.

Income: The target audience for CRED consists of high-income individuals. This group is characterized by a significant earning capacity, which aligns with their ability to manage multiple credit cards and take advantage of CRED's rewards and benefits.

Occupation: CRED's target customers are predominantly professionals. These could include individuals with various occupations such as IT professionals, managers, entrepreneurs, and other career-focused individuals who rely on credit cards for their financial transactions.

Location: CRED primarily focuses on urban areas. Urban locations often have higher credit card penetration rates and access to premium services, making them an ideal market for CRED's offerings.

Credit Score: CRED refines its customer base by requiring a minimum credit score of 750 or more. This criterion ensures that the user base consists of individuals with a strong credit history and good creditworthiness.

BRANDING:

CRED has successfully established a strong brand presence and sustained it through strategic initiatives. CRED's brand strength is a key driver of its success. It has cultivated a robust brand identity around its app and services. This strong brand image helps attract new users and retain existing ones. Users associate CRED with trustworthiness and reliability in the credit card management space.

Additionally, CRED's brand is bolstered by its attractive rewards program. The company offers enticing incentives such as cashback, discounts, and early access to events. These rewards serve as powerful motivators for users to sign up for the app and actively engage with its services.

BUSINESS MODEL

CRED, the innovative financial management application, extends its services beyond bill payments and rewards, offering users a suite of tools for credit card spend tracking and management, along with insightful analyses of their spending habits and card usage efficiency.

CRED Rewards System: CRED operates a unique rewards system where users are incentivized to pay their credit card bills through the app. This strategy fosters user loyalty as they accumulate CRED coins, which can be redeemed for exclusive rewards within the platform.

Business Partnerships: CRED’s partnerships with a diverse range of businesses enable it to provide enticing deals to users. These collaborations create a symbiotic relationship, enhancing user experience while boosting visibility for partner businesses.

Listing Fees: One of CRED’s revenue streams comes from receiving fees from businesses every time a user redeems Cred coins for offers. This fee structure reflects the value CRED brings to the table by connecting engaged users with businesses.

Data Monetization: CRED prudently collects and safeguards users' financial data. Banks and credit card companies recognize the worth of this anonymized and aggregated data and are willing to pay for access, leveraging it to shape their financial services.

CRED's business and revenue model is a testament to its commitment to promoting financial wellness while fostering growth and profitability for both users and business partners.

COST ANALYSIS (FINANCIALS)

In the realm of financial analysis, it's crucial to understand how credit risk is assessed, as it plays a significant role in the operations of a platform like CRED. Drawing insights from the principles of credit risk analysis from reputable sources like Corporate Finance Institute, Wikipedia and Wall Street Prep, we can shed light on CRED's financial standing.

Credit Risk Analysis: CRED, as a platform dealing with credit card payments and rewards, is inherently exposed to credit risk. Credit risk analysis involves weighing the costs and benefits of taking on credit risk, which aligns with CRED's business model. The company must measure, analyze, and manage the risks it's willing to accept in its pursuit of rewarding users for paying their credit card bills.

Financial Ratios: To gauge CRED's financial health, one would need to analyze financial ratios. These ratios provide a snapshot of the company's liquidity, profitability, and leverage. Understanding these ratios can help assess CRED's ability to manage its operations effectively and sustain its business model.

Debt Covenants: Debt covenants are contractual agreements that dictate how a company manages its financial affairs, especially when it has borrowed funds. Analyzing CRED's debt covenants, if any, can provide insights into how the company manages its financial obligations and the impact on its financial stability.

Credit Metrics: Credit metrics are essential for evaluating the risk associated with a company's creditworthiness. CRED, in its engagement with users and businesses, must maintain a solid credit profile to ensure trust and reliability. Examining credit metrics can help understand how CRED manages its credit risk exposure.

Funding and Valuation

CRED has successfully raised significant funding from various investors. The company's valuation has increased significantly over several funding rounds:

In its Series A round, CRED raised $636K.

Series B brought in $120M, marking a substantial increase of $450 million.

The Series C funding amounted to $81M, further increasing its valuation by $806 million.

CRED's Series D saw an investment of $215M, raising its valuation to $2.2 billion.

Series E brought in $251M, pushing its valuation to $4.01 billion.

Notably, in the Series F funding, CRED raised $80 million, valuing the company at approximately $6.4 billion.

Financial Performance

CRED reported losses of ₹360.31 crore in the 2020 fiscal year (FY20). These losses were primarily attributed to high expenditures on marketing and advertising.

Product Expansion

As of April 2021, CRED offered a range of products, including CRED RentPay, CRED Cash, CRED Pay, CRED Store, and CRED Travel Store. In August 2021, the company launched CRED Mint, a Peer-to-Peer (P2P) lending feature aimed at monetizing its user base.

By delving into these aspects of credit risk analysis, one can gain a deeper understanding of CRED's financial position and its ability to sustain its unique business model that rewards users for responsible credit card bill payments. Financial analysis is a cornerstone for evaluating the stability and growth potential of a company like CRED in the dynamic fintech landscape.

USER PERSONA

User Persona 1:

Name: Karthik Srinivasan

Age: 30

Occupation: Sales Executive

Location: Chennai

About:

Karthik is a 30-year-old sales executive living in Chennai. Karthik is focused on his career and rarely gets enough time to sort out his finances, expenses and bill payments. He prefers to have a digital app manage the bill payments for him or at least actively remind him of the due payment.

Goals:

Efficiently manage his monthly budget and track expenses

Stay on top of his credit card payments and avoid late fees or penalties

To have a secure and trustworthy payment solution

Pain Points:

Difficulty in budgeting and tracking expenses, leading to overspending

The tedious process of managing and paying recurring bills

User Persona 2:

Name: Priya Deshmukh

Age: 28

Occupation: Software Engineer

Location: Pune

About:

Priya, a 28-year-old software engineer, resides in Pune. Priya enjoys exploring new technologies and is passionate about eco-friendly initiatives. Also, she actively seeks rewards for payment done or inviting friends to use a certain fintech platform

Goals:

Efficiently manage her monthly budget and reduce expenses

Actively seek ways to earn and redeem rewards effectively, especially for travel expenses

Pain Points:

Difficulty in tracking and minimizing her monthly expenses

Lack of clarity on how to optimize rewards and maximize benefits across her credit cards

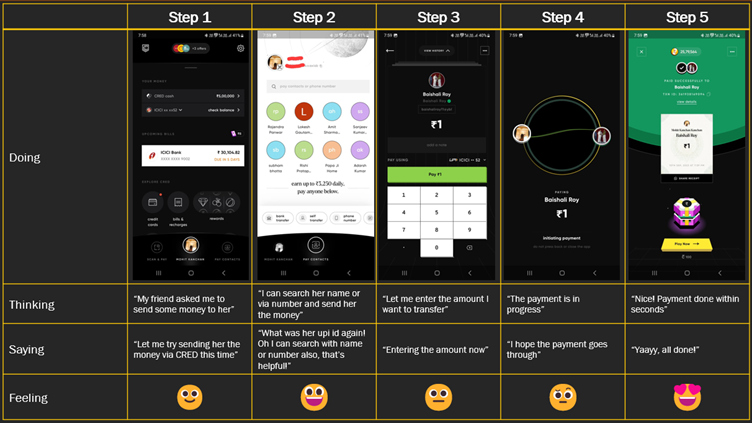

CUSTOMER JOURNEY MAP

COMPETITIVE ANALYSIS

CRED's Unique Offering:

CRED primarily targets credit card users, offering them a simplified way to manage and pay credit card bills.

It differentiates itself by providing rewards to users for timely payments, which can be redeemed for exclusive discounts.

Key Competitors:

Paytm: A fintech giant with a diverse range of financial services, including digital payments, mobile recharges, and e-commerce. Paytm boasts a large user base and extensive offerings.

PhonePe: Known for its UPI-based transactions and digital payment services, PhonePe provides a user-friendly experience, making it a significant competitor.

BharatPe: Focusing on merchant payments, BharatPe offers solutions like QR code-based payments and tailored loans for small businesses. It competes by addressing specific merchant needs.

Google Pay: Google Pay, backed by the tech giant Google, is a digital wallet and payment app. Its brand recognition and technological capabilities make it a formidable competitor.

RECOMMENDATIONS

Streamlined P2P Payments: Implement biometric authentication options like fingerprint or face ID for P2P payments. This would not only enhance security but also make transactions more convenient. Alternatively, allows users to save their PINs for P2P payments, reducing the need for repetitive PIN entry.

Expand Cashback and Discounts: Forge partnerships with a wider array of merchants to diversify cashback and discount opportunities. Increasing the cashback and discount percentages would further incentivize users to make payments through the app.

Enhance App Performance: Invest in improving the app's performance and user-friendliness. Ensuring the app runs smoothly and efficiently will make it a more attractive and reliable payment option for users. Expanding the network of supported stores and businesses will also increase its utility.

Personalized Offers: Tailor cashback and discount offers to individual users based on their preferences and spending patterns. Personalization can significantly increase user engagement and satisfaction.

Diversify Rewards: Provide multiple avenues for users to earn rewards, such as watching videos, participating in surveys, or referring friends. This gamification approach can make the app more engaging and encourage more frequent usage.

Optimize Contacts: Simplify contact management within the app. Save business or merchant contacts separately from personal contacts. Include a category for business contacts, making it easier for users to access and pay merchants.

Improved User Interface: Enhance the user interface by revising the microcopy and optimizing the search bar for a more user-friendly experience. Additionally, improves the visibility and organization of transaction history for easy reference.

By implementing these recommendations, CRED can not only elevate its user experience but also strengthen its position in the competitive fintech landscape. These enhancements would likely attract more users and encourage existing ones to use the app more frequently, driving its growth and success.

KEY METRICS

North Star Metrics:

Transaction Amount/ day

Number of transactions/ day

L1 Metrics:

MAU

DAU

CLV

Conversion Rate

L2 Metrics:

Play Store or App Store Rating

NPS

Number of rewards user/ month

Number of users who spent CRED coins/ month

CONCLUSION

In this CRED product teardown, we've dissected the various facets of this Indian credit card payment app. CRED has undeniably made a significant impact in the Indian fintech space with its unique approach of rewarding credit card users. With a focus on convenience, rewards, and financial management, it has successfully carved a niche for itself.

Key highlights from our analysis include its distinct business model, strategic partnerships with premium brands, and steady growth in a competitive landscape. While facing competition from industry giants like Paytm, PhonePe, and Google Pay, CRED's specialization in credit card management sets it apart.

As CRED continues to evolve and expand, it will be intriguing to see how it navigates the ever-changing fintech landscape and whether it can maintain its unique value proposition in the years to come.